Intelligent Process Automation (IPA) for streamlined insurance underwriting management

Introduction Insurance Underwriting and its management is a crucial department in the Insurance industry as it helps determine appropriate pricing for the correct risks associated with businesses. However, manual underwriting risk assessments are time-consuming, prone to errors, and may cause information loss. In fact, according to Accenture, more than 50% of an average underwriter’s workday is…

Introduction

Insurance Underwriting and its management is a crucial department in the Insurance industry as it helps determine appropriate pricing for the correct risks associated with businesses. However, manual underwriting risk assessments are time-consuming, prone to errors, and may cause information loss. In fact, according to Accenture, more than 50% of an average underwriter’s workday is spent on repetitive tasks such as processing detailed information about different kinds of risks [1]. To mitigate the challenges presented by manual risk assessments, insurance underwriting with intelligent automation can do wonders in Underwriting Management operations and digitally streamline them.

This is possible by incorporating AI-based Intelligent Process Automation (IPA) to achieve end-to-end processing of underwriting activities in the insurance industry. This blog talks about intelligent automation in the form of IPA for underwriting and discusses the various aspects of this technology.

Effects of slow conventional underwriting processing on customer support for Insurers

The data processed in underwriting management is received through a variety of formats such as photographs, emails, pdfs, etc. from different external sources and systems. These formats mainly comprise unstructured data or free-text data, which could be highly disorganized and vary in their structure on a case-to-case basis.

As a result, conventional automation techniques and manual ways find it challenging to process this data with high accuracy as their software frameworks are not equipped well enough to handle large volumes of unstructured data. Moreover, processing this data is highly repetitive and monotonous, which consumes long time durations for employees.

These actions ultimately become detrimental to an insurer’s cost-efficiency, result in reduced work productivity, and lengthen the wait times of customers of insurance companies [3]. This can hamper customer satisfaction to a large extent negatively and insurers could start losing their customer base as a result. These challenges might also affect other insurance business functions such as claims handling, customer service, invoice management, and document archival.

How does IPA-based underwriting automation work in the insurance industry?

Intelligent Process Automation is a collection of technologies powered by Artificial Intelligence that can automate, integrate, and process a variety of digital business operations through different platforms. IPA for underwriting can automate the entire chain of processes in the field thus providing end-to-end automation support.

- IPA solutions in underwriting can collect, read, and identify different types of data received from both external and internal sources related to risks and liabilities.

- The solutions then extract relevant information from this data which might be structured as well as unstructured (free-text) and use this data to trigger certain business rules.

- These business rules together with decision engines are used to perform different business functions such as classification, replying and forwarding, authentication, and archival to name a few.

- The IPA solutions can overall access, organize, and analyze the data to gain valuable insights about creating the appropriate insurance policy for customers.

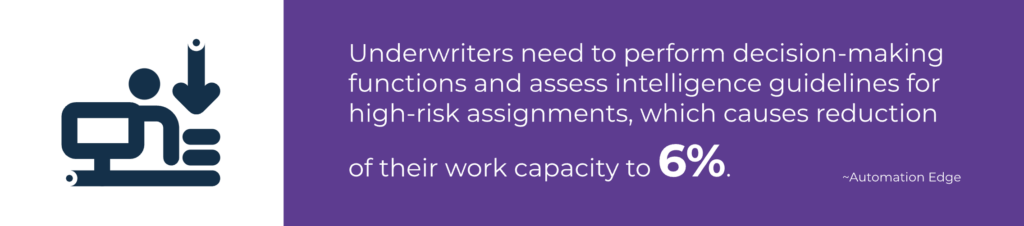

Not all business functions can be automated by using IPA and in some cases that deal with complex policy-making or sensitive insurance underwriting, a human touch is still required. In fact, according to Automation Edge, underwriters are still required to perform their decision-making functions and assess intelligence guidelines for high-risk assignments, resulting in a reduction of underwriting work capacity to 6%, rather than 60% or even higher [3]. This indicates that human and digital IPA solutions can work together, with the latter forwarding complex cases to humans for resolution.

Overall benefits of IPA for automated insurance underwriting

End-to-end automation of processes – helps streamline the customer journey

High process completion speed – Takes minimal time for completing tasks

Freeing up time for employees – Saves valuable time for employees from repetitive tasks

Reduce risks of errors and mistakes – Robust action flow and rules reduce errors drastically

Satisfy customer requirements – Understand customer behavior for an improved experience

Efficient resource utilization – Allows for more effective use of resources for insurers

Enhanced user accessibility – Enables a centralized system for quick user access

Improved ROI and profits – Boost Return on Investment by scaling without more staffing

[4]

Work areas in underwriting practices that can benefit from IPA

Insurance risks for properties and liabilities in different commercial domains vary depending on the product or service being offered. For example, insurance risk evaluation for automobiles is based on the type of vehicle, fueling mechanism, financial capacity of the customer, brand, etc. Whereas for air travel insurance, the liabilities considered are the airline company, the region being visited, health illnesses, and so on. Based on these liabilities and the associated processes involved, there are five categories of activities managed by underwriters in insurance.

Intake

This step deals with the collection of data from multiple sources and its processing by underwriters manually in traditional underwriting practices. IPA can be used at this stage for automated data capturing, extraction, and delivery for further risk assessment using AI-fueled technologies such as Optical Character Recognition (OCR) and Intelligent Document Processing (IDP).

Triaging

At this stage, the extracted data is subjected to careful evaluation and is assessed for the risks it might carry. IPA can be applied for triaging with the help of specifically developed business rules and logic to categorize the information and bring the customer closer to the right insurance products or service offerings. At this step, Artificial Intelligence through IPA can be leveraged extensively to automate the simpler and more common forms of evaluations to reduce the workload of the underwriters. With the right AI training, IPA can speed up triaging, enable underwriters to work on more complex policies and move along the entire process faster.

Pricing

The third step involves building up pricing models based on the risk factors used for triaging. Over here, the application of AI and Machine Learning through Intelligent Process Automation is highly valuable. IPA enables the pricing of hundreds or thousands of similar risk factors and forming pricing models and concrete insurance policies for customers of insurance companies based on their applications. This reduces the customer queue by offering them policy pricing at a fast pace.

Processing

The last stage deals mainly with processes related to tracking and managing risk-related data and processing it into desired formats for policy underwriting and further claims-related processes. Traditional Intelligent Process Automation can work at the back end at this stage and perform administrative functions effectively and rapid completion of underwriting actions, especially in the case of simple policies.

Conclusion

We saw how Intelligent Process Automation can do wonders for insurance underwriters and make their work more efficient and fast-tracked. Before choosing an IPA solution to automate underwriting processes, businesses need to consider a few factors.

- Identify the key and secondary challenges to resolve using AI and automation.

- Prepare a list of goals that align with these challenges and have an output or results.

- Research AI solution vendors that provide IPA solutions and check if their services match business requirements.

- Connect with the vendor representatives for a demo of the solution and gather feedback and information.

- Identify a pathway by which the IPA can ultimately improve the customer experience for a business by tackling the challenges and achieving the goals outlined. [5]

From an overall perspective, Intelligent Process Automation solutions can automate repetitive and time-consuming underwriting activities and improve task productivity for underwriters and actuaries. The freed-up time can then be used on more demanding and sensitive tasks that are highly complex in nature.

Insurers can adopt intelligent automation through IPA in various ways, the chief of which is a digital assistant that can work in real-time, can understand and interpret human communication, and be configured as per business requirements with different product modules.

How do Simplifai AI solutions enhance business operations in the insurance industry

Simplifai is an AI solutions company that provides end-to-end automation for businesses in the Insurance sector through AI-powered Digital Employee solutions.

Digital Employees for Insurance are quick to implement, read and interpret structured and unstructured data, and help scale up organizational growth. They can be easily deployed in business functions and departments such as insurance underwriting, claims handling, customer service, document archival, premium payments handling, invoice and bill processing, and many more in this industry.

Digital Employees comprise individual modules such as Emailbot, Documentbot, and Chatbot, which collectively provide Intelligent Process Automation (IPA) for insurance businesses. Together with Natural Language Processing (NLP), decision engine, rules engine, our solutions can be integrated with external, third-party systems with Robotic Process Automation (RPA) and Application Programming Interface (API).

Curious to know how our Digital Employee for Insurance works? Click the button below:

Know more about our Digital Employee Solutions for Insurance

Sources:

[1] Mertzel, K. Improve Insurance Underwriting with Intelligent Automation. RPA Thought Leadership. Automation Anywhere (Jan 20, 2021), https://www.automationanywhere.com/company/blog/rpa-thought-leadership/improve-insurance-underwriting-with-intelligent-automation

[2] Automation Takes Over the Risks of Underwriters to Create a Stout Loan Management System. Banking & Insurance, IT Automation (Oct 11, 2021), https://automationedge.com/blogs/automation-takes-over-the-risks-of-underwriters-to-create-a-stout-loan-management-system/

[3] Intelligent Process Automation in Insurance, Hexaware (2019) https://hexaware.com/wp-content/uploads/2019/10/Intelligent-Process-Automation-in-Insurance.pdf

[4] Top 5 Advantages of Using Automated Underwriting, Origin Affinity (Feb 9, 2022), https://www.originaffinity.com/top-5-advantages-of-using-automated-underwriting/#:~:text=Top%205%20Advantages%20of%20Using%20Automated%20Underwriting%201,Consistency%20…%205%205.%20Boost%20Profit%20Margins%20

{kind=link}

{kind=link}